IMPORT TARIFFS - LATEST NEWS & UPDATES

In This Article:

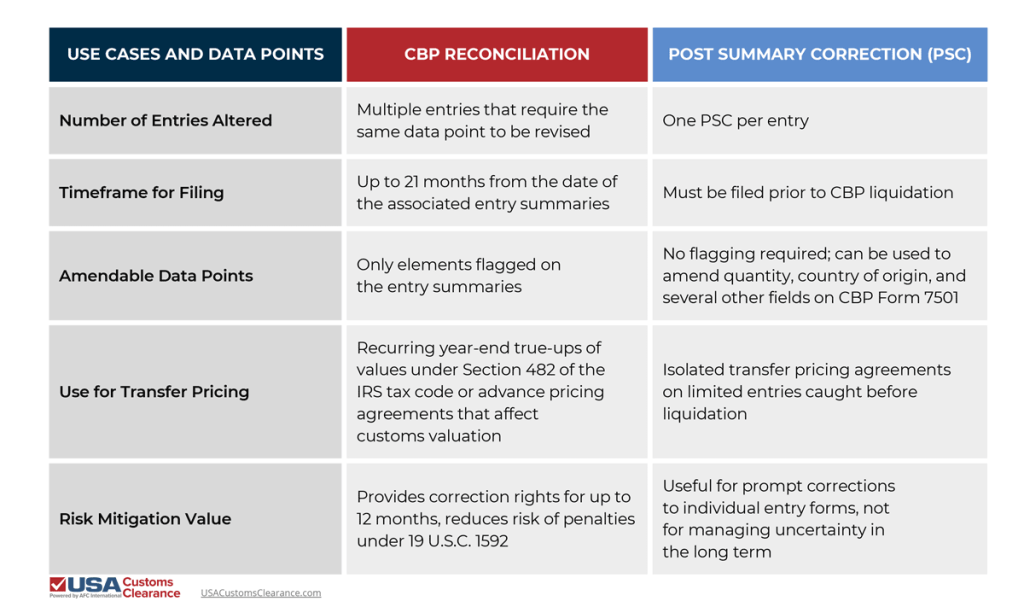

A U.S. Customs and Border Protection (CBP) reconciliation entry is a voluntary post-import customs process that allows importers to finalize uncertain elements, such as transfer pricing adjustments, after goods enter the U.S. while maintaining compliance with CBP valuation rules and Section 482 of the Internal Revenue Code's arms-length requirements. Importers who have to make adjustments to multiple entries may benefit from using the reconciliation process rather than post-summary corrections (PSC).

Key Takeaways

Our guide explains the CBP reconciliation process in detail, contrasting it with other post-release processes.

Our Expert Licensed Customs Brokers take whatever has changed (value, HTS, origin, AD/CVD, transfer pricing, etc.) and confirm whether a CBP Reconciliation Entry or a Post Summary Correction (PSC) is the safest, fastest path—so you don’t miss deadlines or trigger avoidable compliance risk.

Confidential initial review — no obligation.

CBP Reconciliation is a voluntary program that allows importers to "flag" elements of their customs import entry for modification at a later date.

Entry types 01, 02, and 06 are eligible for reconciliation after clearance.

To use the CBP reconciliation process, an importer must have a continuous customs bond on file with a reconciliation rider. The importer must also flag those elements of the entry summary that may require correction after clearance and release of the associated shipment.

The reconciliation process can be used to amend the following data points after customs clearance:

When filing a reconciliation entry, you have 12 months from the date of importation to correct FTA information and 21 months from the date of the entry summary to correct value, classification, and the 9802 status of the imported merchandise.

What Reconciliation does not do: A Reconciliation filing only corrects the specific element(s) you flagged on the underlying entry summaries. If you did not flag the element, you generally cannot use Reconciliation later to change it, and you may need to consider PSC, a protest, or other remedies depending on liquidation status.

Using CBP’s reconciliation program can be broken down into three basic steps: flagging, filing, and getting refunded (or paying additional duties when necessary). Let’s look at each step in detail.

If you believe it will be necessary to file for reconciliation on an entry summary or summaries, your first step is to flag the entry itself. You’ll need to flag the specific elements of the summary that could need reconciliation. For instance, flagging an entry for a possible value change after clearance only permits you to amend the value field, not the FTA eligibility field.

Within the 12 months permitted for amendments to FTA eligibility or 21 months for valuation, classification, and 9802 status of your imported goods. One reconciliation entry can be used to reconcile multiple entry summaries, but only for one type of data field.

If you need to reconcile valuation and FTA status on multiple entries, you’d need to file at least one reconciliation for the valuation changes and another for FTA eligibility.

Depending on whether you underpaid or overpaid duties based on the information amended by reconciliation, you’ll need to either remit payment to CBP for the balance owed or wait for the overpaid amount to be refunded.

As of February 2026, CBP requires the vast majority of importers to have an Automated Commercial Environment (ACE) account to receive refunds via ACH deposits. Paper checks are only available for limited scenarios, such as high-security transactions.

Importers can use reconciliation and post-summary corrections to make post-clearance changes to their customs entries. Knowing when to choose reconciliation to amend your entries is a key element of compliant customs documentation.

International companies that routinely true up their transfer pricing between different segments of their business benefit from reconciliation over individual entry corrections. This is because transfer pricing adjustments are predictable to an extent and usually apply to several entries rather than one or two.

For instance, if you undervalued a good on multiple entries consistently and discover the mistake during an audit, a single reconciliation entry can be used to amend the value of multiple 7501 forms, as long as those entries were originally flagged for reconciliation.

Another scenario that can be resolved via reconciliation is making mass adjustments to entries due to a pending CBP binding ruling decision. If CBP determines that goods were imported under an incorrect HTS code, it will likely lead to a change in duties owed on the affected merchandise across multiple entries.

Our Expert Licensed Customs Brokers map your required data, timelines, and who needs to supply what—so your reconciliation package is complete and defensible.

Confidential initial review — no obligation.

Transfer pricing adjustments aren’t the only reason a well-intentioned importer could undervalue an import. It’s also easy to overlook dutiable assists and their impact on the value of an imported product.

Example: Let’s say you request technical drawings of a piece of custom machinery before it's manufactured. If you paid $1,000 for those drawings and then proceeded with the order, the thousand dollars count toward the value of the finished product and should be included in your valuation.

Reconciliation allows you to make those valuation adjustments across multiple entries, even after CBP liquidation.

When a domestic business claims “critical circumstances” during an anti dumping/countervailing duty (AD/CVD) investigation, CBP is authorized to retroactively collect AD/CVDs on entries up to 90 days before the initial findings are published.

Make sure you flag any products you order that are under AD/CVD investigations for possible reconciliation, as you may end up owing retroactive increased duties if the investigation ends in an AD/CVD order, which involves determinations from the U.S. Department of Commerce and U.S. International Trade Commission (USITC).

A post-summary correction (PSC) is an option CBP offers importers to change information on a single entry summary (CBP Form 7501) that has not been liquidated. In the following table, I’ve compiled information about both processes to help importers quickly decide which one will work best for a given importing situation.

Reconciliation entries allow importers to make adjustments to several entry forms at once, but there are scenarios in which a PSC is more effective.

Post-summary corrections are a better choice than reconciliation in the following scenarios:

Some of the most common mistakes made by new importers can be easily solved via PSC.

If your entries were filed by a customs broker, the broker can use Automated Broker Interface (ABI) software to quickly submit reconciliations for multiple entries. A customs broker’s experience in customs clearance also provides insights new and even experienced importers overlook.

A Licensed Customs Broker can help you:

CBP’s documentation requirements and regulatory requirements are best navigated with the assistance of an experienced customs broker.

What we do:

Typical timeline: We can usually review your situation and advise the correct filing path the same business day. Filing timelines depend on your documentation readiness, ACE flagging status, and whether entries are still unliquidated or require consolidation and final data.

What you’ll need: Entry numbers and/or CBP Form 7501s, commercial invoices, packing lists, broker/ABI data, HTS classifications used, origin documentation, FTA/USMCA support, transfer pricing adjustment documentation, assists/royalty details, and bond details.

Why choose us: We are licensed customs brokers who handle post-entry corrections and reconciliation strategy as part of compliant clearance, helping importers choose the right tool, meet deadlines, and avoid avoidable duties, penalties, and rework.

Outcome: Your entries are corrected using the appropriate CBP process, filed within required time windows, and supported with documentation that stands up to CBP review so you can minimize duty surprises, reduce compliance risk, and keep your import program audit-ready.

Call us at (855) 912-0406 to start simplifying your importing process today.

Q: Can I file reconciliation if I did not flag the entry?

A: No, reconciliation can only be used to amend properly flagged customs entries.

Q: How long do I have to file a reconciliation entry?

A: Up to 12 months from importation for amending FTA information, up to 21 months for changes to valuation and other flagged elements of the entry form(s).

Q: Does reconciliation stop liquidation?

A: It does not, although the liquidation of a reconciliation can be protested.

Q: Is reconciliation required for transfer pricing adjustments?

A: Reconciliation is the best option available for mass valuation amendments that result from adjustments to transfer pricing.

Copy URL to Clipboard

Copy URL to Clipboard

Did you find this article helpful?

See more of our coverage on Google.

Add usacustomsclearance.com as a preferred source!

Add usacustomclearance.com as a preferred source!

See more of our coverage in Google's Top Stories.

Licensed customs support for importers across a wide range of U.S. entry needs. USA Customs Clearance provides Customs Bonds, Consulting, Customs Brokerage, Manifest Confidentiality, Importer of Record support, and Guides & Resources to help importers prepare for U.S. Customs and Border Protection (CBP) requirements and customs clearance with regulatory compliance, greater clarity, and confidence.

With licensed broker support, transparent service information, and secure checkout, we help importers take the right next step.

Add your first comment to this post